Backtest Like a Pro with a Forex API

06 December 2024

The financial markets are fast-paced, making them instrumental in accessing reliable data for building and testing trading strategies. Seamlessly integrating high-quality data into backtesting frameworks is invaluable for traders and analysts. TraderMade APIs provide traders and analysts with this capability by delivering accurate, granular, and comprehensive market data.

This article uses TraderMade's Time Series API to access historical data, implement a simple moving average (SMA) crossover strategy, and backtest its performance.

What is an SMA Crossover Strategy?

A moving average crossover strategy is a basic yet powerful technical analysis method. It involves tracking two SMAs:

1) A short-term SMA, which reacts more quickly to price changes.

2) A long-term SMA smoothens out short-term fluctuations.

When the short-term SMA crosses above the long-term SMA, it generates a buy signal, indicating upward momentum. Conversely, when the short-term SMA crosses below the long-term SMA, it generates a sell signal, suggesting downward momentum.

Data Collection

Start by installing TraderMade's SDK as follows:

!pip install tradermade

We use the installed SDK to fetch hourly time series forex data. The following Python code illustrates how to fetch currency pair EUR/USD data.

import tradermade as tm

import pandas as pd

def fetch_forex_data(api_key, currency, start_date, end_date, interval="hourly", fields=["open", "high", "low", "close"]):

# Set API key

tm.set_rest_api_key(api_key)

# Fetch the data

data = tm.timeseries(currency=currency, start=start_date, end=end_date, interval=interval, fields=fields)

# Convert data directly to DataFrame

df = pd.DataFrame(data)

# Convert 'date' column to datetime

df["date"] = pd.to_datetime(df["date"])

# Set 'date' as the index

df.set_index("date", inplace=True)

return df

# Adjust as needed

api_key = "YOUR TRADERMADE API KEY"

currency = "EURUSD"

start_date = "2024-11-01-00:00"

end_date = "2024-11-27-05:12"

# Fetch the data and display the first few rows

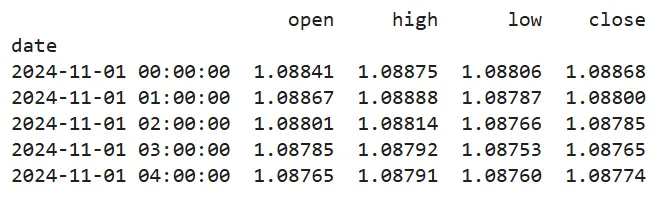

forex_data = fetch_forex_data(api_key, currency, start_date, end_date)

forex_data.head()

The data has been successfully fetched and preprocessed for Backtesting.

Implementing a Simple SMA Crossover strategy and Backtesting

This section uses the backtesting Python library to define and test our SMA crossover strategy. Here's a little background about the backtesting library for those who haven't heard about it. It's one of the most powerful and reliable Python frameworks for backtesting technical strategies such as SMA crossover, RSI crossover, Mean-reversal strategies, Momentum strategies, and more.

import numpy as np

from backtesting import Backtest, Strategy

from backtesting.lib import crossover

from backtesting.test import SMA

# Define the SMA crossover trading strategy

class SMACrossoverStrategy(Strategy):

def init(self):

# Calculate shorter-period SMAs for limited data

price = self.data.Close

self.short_sma = self.I(SMA, price, 20) # Short window

self.long_sma = self.I(SMA, price, 60) # Long window

def next(self):

# Check for crossover signals

if crossover(self.short_sma, self.long_sma):

self.buy()

elif crossover(self.long_sma, self.short_sma):

self.sell()

# Initialize and run the backtest

df = forex_data

df.rename(columns={"open": "Open", "high": "High", "low": "Low", "close": "Close"}, inplace=True)

bt = Backtest(df, SMACrossoverStrategy, cash=10000, commission=.002)

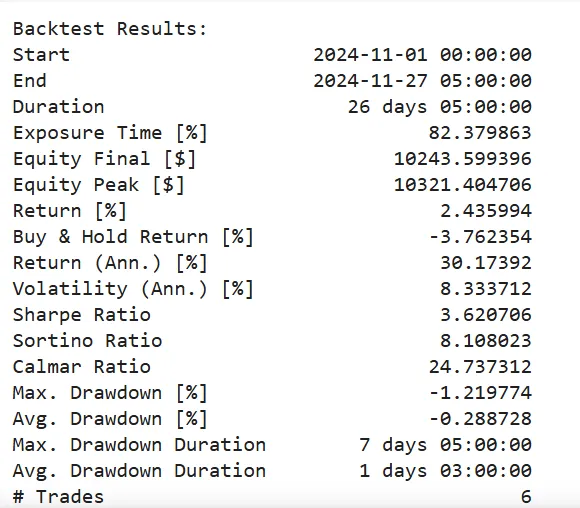

result = bt.run()

# Display the backtest results

print("Backtest Results:")

print(result)

The strategy involves tracking two moving averages: a 20-period and a 60-period SMA. When the short SMA crosses the long SMA, it triggers a buy order. Conversely, when it crosses below, it triggers a sell order. Within 25 days, the simple strategy made a profit of $243 from 6 trades.

Equity and SMAs Curve

The Python code below evaluates the performance of the SMA crossover strategy. SMAs help visualize the price trends and the points of crossover that generate buy/sell signals. The equity curve helps evaluate the strategy's performance, showing how these signals affect portfolio growth.

Combining the two curves helps to easily observe how the crossover events correlate with the changes in portfolio value, providing critical insights into the efficacy of the SMA crossover strategy.

Plotly visualizes the equity and SMAs curves helping traders assess their strategy's profitability.

import plotly.graph_objects as go # Plot equity curve and SMAs using Plotly import plotly.graph_objects as go fig = go.Figure() # Add equity curve equity_curve = result['_equity_curve'] fig.add_trace(go.Scatter( x=equity_curve.index, y=equity_curve['Equity'], mode='lines', name='Equity Curve', yaxis='y1' # Link to first y-axis )) # Add price with SMAs on a secondary y-axis fig.add_trace(go.Scatter( x=forex_data.index, y=forex_data['Close'], mode='lines', name='Close Price', yaxis='y2', # Link to second y-axis line=dict(color='blue') )) fig.add_trace(go.Scatter( x=forex_data.index, y=forex_data['Close'].rolling(window=20).mean(), mode='lines', name='Short SMA (20)', yaxis='y2', # Link to second y-axis line=dict(color='orange', dash='dash') )) fig.add_trace(go.Scatter( x=forex_data.index, y=forex_data['Close'].rolling(window=60).mean(), mode='lines', name='Long SMA (60)', yaxis='y2', # Link to second y-axis line=dict(color='green', dash='dash') )) # Customize layout with two y-axes fig.update_layout( title="Equity Curve and SMAs (SMA Crossover Strategy)", xaxis_title="Date", yaxis_title="Portfolio Value ($)", # For equity curve yaxis=dict(title="Equity ($)", side="left"), yaxis2=dict(title="Price and SMAs", overlaying="y", side="right"), # For price and SMAs template="plotly_dark", showlegend=True ) # Show the plot fig.show()

Final Thoughts

In conclusion, Backtesting requires accurate, high-frequency data, and TraderMade's APIs make this seamless. Whether you are a beginner experimenting with various strategies or a seasoned analyst building complex models, the company's products empower you with the appropriate tools.

Are you ready to integrate TraderMade's APIs into your workflow? Get started today and bring your ideas to life!